When and How to Plan for Selling Your Business: Key Considerations for a Successful Exit

Selling a business is one of the biggest financial and personal decisions an owner will ever make. Whether your business has been your life’s work or a venture you’ve grown to a certain stage, the sale can be both exciting and overwhelming. The key to maximizing value and ensuring a smooth transition lies in planning early and strategically.

When Should You Start Planning to Sell?

Many business owners wait until they’re “ready” to sell before thinking about an exit strategy. The truth is, the best time to start planning is 3–5 years before you intend to sell. Why? Because preparing in advance allows you to:

- Maximize Value: Address inefficiencies, clean up financials, and strengthen operations.

- Increase Buyer Appeal: Buyers want businesses that are easy to transition and not overly dependent on the owner.

- Reduce Surprises: Advanced planning helps you anticipate and resolve issues before they arise during due diligence.

- Tax Optimization: Structuring the business and personal finances in advance can save you significant taxes on the sale.

How to Prepare for Selling a Business

- Get a Professional Valuation

Understanding what your business is worth now—and what drives that value—helps you set realistic expectations and uncover areas to improve. - Strengthen Financial Records

Clean, accurate, and detailed financial statements are essential. Buyers want transparency, and sloppy books can reduce value or kill a deal. - Reduce Owner Dependence

If the business relies heavily on you, buyers may see higher risk. Build systems, delegate responsibilities, and strengthen your management team. - Diversify Revenue Streams

Businesses with one major client or product line are riskier. Work on spreading out your income sources to make the business more resilient. - Review Legal and Compliance Matters

Ensure contracts, licenses, intellectual property, and employment agreements are in order. Buyers don’t want hidden liabilities. - Tax and Exit Planning

Work with an accountant and advisors to structure the sale in a way that minimizes taxes and aligns with your long-term wealth goals. For example, you may consider stock vs. asset sales, installment sales, or estate planning strategies. - Identify Potential Buyers

Depending on your goals, your ideal buyer might be a competitor, private equity group, employee, or family member. Each has unique considerations for structure and transition. - Plan Your Role After the Sale

Some buyers will want you to stay on for a transition period. Decide in advance how long you’re willing to remain involved and in what capacity.

Things to Consider Before Selling

- Timing: The economy, interest rates, and industry trends can impact the value of your business.

- Emotional Readiness: Many owners underestimate how attached they are to their businesses. Be prepared for the personal side of letting go.

- Post-Sale Life: What will you do after the sale—retire, start another business, or shift to advisory work? Knowing your “what’s next” is critical.

- Team & Legacy: If your employees, clients, or community impact matter to you, consider how the sale will affect them and choose a buyer accordingly.

Final Thoughts

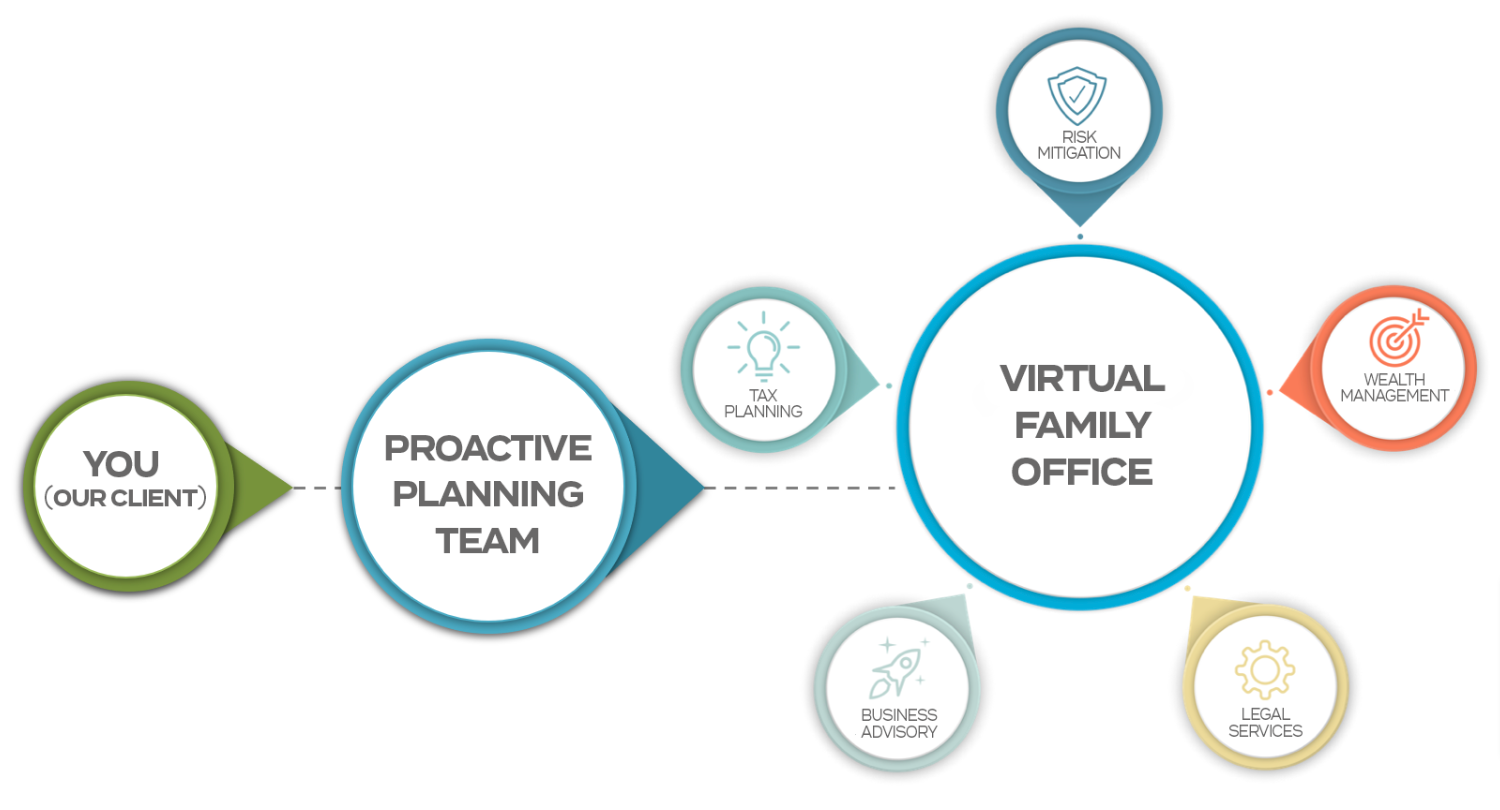

Selling your business isn’t just a financial transaction—it’s the culmination of years of work and the start of a new chapter. By starting early, getting the right advisors, and carefully preparing your business, you’ll not only maximize the financial return but also create peace of mind knowing your legacy is in good hands. The Hammernik & Associates Virtual Family Office experience allows for proactive planning, which includes business development and planning for a potential business exit. This is one of the many great features that our Virtual Family Office client are able to take advantage of through our services.

See More Blog Posts